- For many non-EU sellers, the real benefit is not only filing support but also having a local point of contact who can respond to tax office letters, document requests, and registration follow-up quickly and in the local language.

5. EU countries where fiscal representation is often required

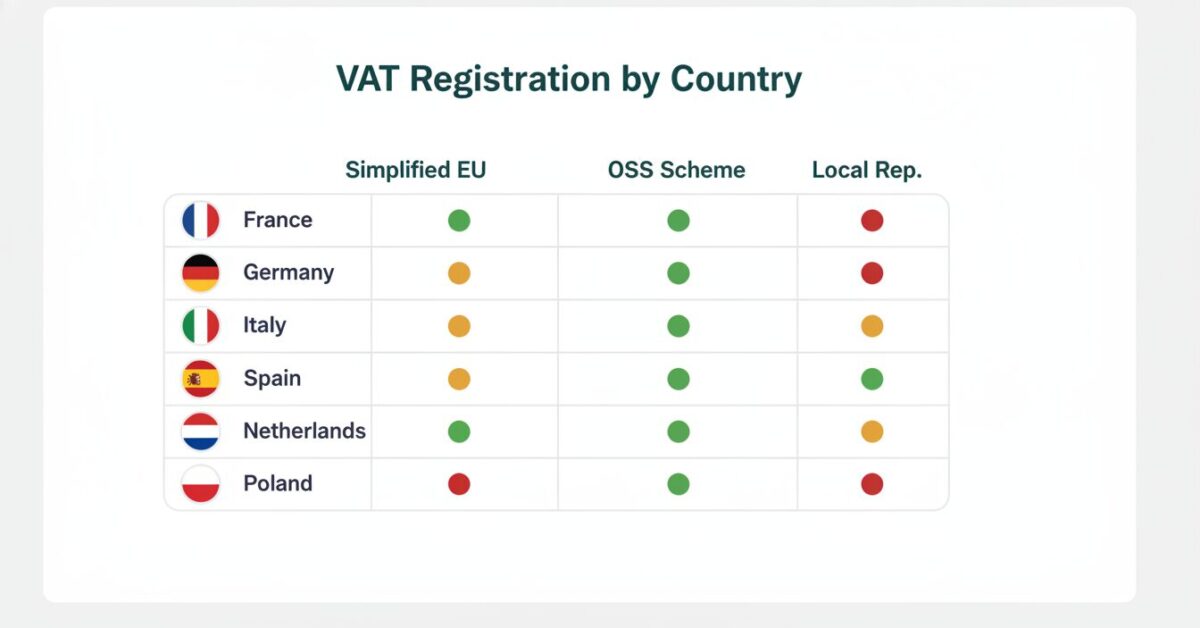

Fiscal representation requirements for non-EU businesses are set at national level, so they must always be confirmed country by country. In practice, several EU Member States often require non-EU businesses to appoint a fiscal representative or local equivalent when registering for VAT, especially where imports or local stock are involved.

Brenda Varela

Last Updated on 2 June 2026- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Denmark

- Estonia

- Greece

- Hungary

- Italy

- Lithuania

- Netherlands

- Poland

- Portugal

- Romania

- Slovenia

- Spain

- Sweden

Germany has a slightly different model—non-EU businesses typically must appoint a tax agent rather than a fiscal representative, although the functions are quite similar. Meanwhile, countries like France, Ireland, Finland, Latvia, Malta, Luxembourg, the Czech Republic, and Slovakia do not always require a fiscal representative, but local rules may still require some form of local agent or direct contact.

Because local rules can change, sellers should verify the current requirement before relying on a historic country list.

It’s essential to verify the requirements of each country because they can change, and exceptions may apply depending on specific business activities.

If your business was built around an Estonian e-Residency structure, it is important to review whether Estonia is still the right place for your VAT registration strategy. Recent rule changes mean many remote-managed companies can no longer rely on Estonia as an easy route to an EU VAT ID, which can also affect where fiscal representation becomes necessary. Our guide to Estonia e-Residency VAT explains what changed, why economic substance now matters more, and what affected businesses should do next.

6. Consequences of Not Having Fiscal representation

Not appointing a fiscal representative (when required) can significantly impact your operations and finances:

- Financial Penalties and Fines

- EU tax authorities impose fines for non-compliance, which can be substantial.

- Any VAT that was paid incorrectly may not be refunded, leading to direct financial losses.

- Operational Roadblocks

- Lack of proper VAT registration could result in rejected applications to sell in certain EU countries.

- Major platforms, suppliers, or manufacturers may refuse to do business with companies that cannot prove compliance with local VAT laws.

- Reputational Damage

- Non-compliance raises red flags with local authorities, which can harm your credibility and relationships with partners in the EU market.

Not sure whether your business needs fiscal representation in the EU or whether another VAT route is enough? hellotax can review your stock locations, imports, and country-specific registration obligations. Speak to our team here.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

7. Administrative Advantages of Fiscal Representation

Simplifying VAT Processes

A fiscal representative deals directly with the tax authorities, managing VAT registration, filings, and any inquiries on your behalf. This centralized approach:

- Accelerates VAT Registration: Often completed more quickly due to established local connections.

- Minimizes Errors: Experts well-versed in local VAT laws reduce the risk of mistakes.

- Keeps You Up-to-Date: They stay current with ever-changing tax regulations, ensuring continuous compliance.

Reducing Administrative Burdens

By offloading VAT-related tasks to a fiscal representative:

- Save Time and Resources: Focus on core business activities, such as marketing and product development, rather than navigating VAT regulations.

- Reduce Risk: Less chance of misreporting or missing deadlines, which could lead to penalties.

- Holistic Approach: Many fiscal representatives offer complementary services like audit support and real-time VAT tracking, ensuring a thorough approach to compliance.

For more information about EU rules on VAT click here.

8. Understanding the Reverse Charge Mechanism

Definition and Application in VAT Compliance

Under the Reverse Charge Mechanism, the responsibility for reporting and paying VAT shifts from the seller to the buyer. This applies mainly to B2B transactions within the EU and is especially relevant if you’re a non-EU business providing services to EU-based companies or selling goods under certain conditions.

- No Need for Multiple Registrations: Because the VAT liability transfers to the buyer, the foreign seller may avoid registering in every EU country where they sell.

- Streamlined Reporting: The buyer records both the input and output VAT, simplifying the seller’s compliance obligations.

Benefits for Non-EU Businesses

- Reduced Administrative Complexity: Minimizes the number of VAT returns you need to file across different EU Member States.

- Cost Efficiency: Eliminates or reduces the need to register in certain markets, saving on administrative fees and ongoing compliance costs.

- Focus on Core Activities: Non-EU companies can concentrate on growth and expansion rather than juggling various VAT systems.

The reverse charge can reduce the number of situations where a supplier needs to account for VAT locally, but it does not remove registration or representation obligations where imports, stock storage, or local taxable supplies still create a VAT footprint.

If your business also makes cross-border B2C sales inside the EU, our guide to One Stop Shop (OSS) explains when OSS can simplify reporting and when local VAT obligations still remain.

9. Conclusion: Drive Growth in the EU Market with the Right Partner

Why Fiscal Representation is a Strategic Must

For non-EU businesses, fiscal representation in the European Union goes far beyond mere compliance. It is a strategic tool that safeguards against penalties, streamlines VAT processes, and ensures seamless interactions with local tax authorities. By choosing the right fiscal representative, you create a solid foundation for sustainable growth within the EU market.

How hellotax Can Help

At hellotax, we specialize in EU VAT compliance for online sellers, with services that include fiscal representation, VAT registration, return filing, and more. We combine professional expertise with user-friendly software solutions to keep your business compliant while reducing administrative burdens.

- Expertise in Multiple Jurisdictions: Our multilingual team understands the nuances of VAT across various EU Member States.

- All-in-One Platform: Manage your VAT registrations, filings, and communications from a single dashboard.

- Personalized Support: Tailored guidance for your specific business model—whether you’re an Amazon FBA seller, a D2C brand, or a niche marketplace vendor.

For a broader operational overview, our EU VAT Compliance Checklist for Online Sellers (2026) shows how registrations, local filings, OSS, stock movements, and tax letters fit together in practice.

Frequently Asked Questions

What is fiscal representation in the EU?

Fiscal representation in the EU means appointing a local representative to help a non-EU business meet VAT obligations such as registration, filing, payments, and tax authority communication.

When is fiscal representation in the EU required?

It may be required when a non-EU business makes taxable supplies in an EU country, imports goods there, or stores stock locally, but the exact rule depends on the Member State.

Does fiscal representation replace VAT registration?

No. Fiscal representation supports or handles VAT compliance, but it does not replace the need for VAT registration where registration is required.

Do all EU countries require fiscal representation for non-EU businesses?

No. The requirement is country-specific, which is why businesses should confirm the current rule in each Member State where they need to register.

Ready to simplify fiscal representation in the EU and reduce VAT risk across multiple countries? hellotax can help you assess where representation is required, manage registrations, and support ongoing compliance. Contact our VAT experts.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

- Having a recognized local fiscal representative fosters trust and often speeds up issue resolution with local tax offices.

- For many non-EU sellers, the real benefit is not only filing support but also having a local point of contact who can respond to tax office letters, document requests, and registration follow-up quickly and in the local language.

5. EU countries where fiscal representation is often required

Fiscal representation requirements for non-EU businesses are set at national level, so they must always be confirmed country by country. In practice, several EU Member States often require non-EU businesses to appoint a fiscal representative or local equivalent when registering for VAT, especially where imports or local stock are involved.

- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Denmark

- Estonia

- Greece

- Hungary

- Italy

- Lithuania

- Netherlands

- Poland

- Portugal

- Romania

- Slovenia

- Spain

- Sweden

Germany has a slightly different model—non-EU businesses typically must appoint a tax agent rather than a fiscal representative, although the functions are quite similar. Meanwhile, countries like France, Ireland, Finland, Latvia, Malta, Luxembourg, the Czech Republic, and Slovakia do not always require a fiscal representative, but local rules may still require some form of local agent or direct contact.

Because local rules can change, sellers should verify the current requirement before relying on a historic country list.

It’s essential to verify the requirements of each country because they can change, and exceptions may apply depending on specific business activities.

If your business was built around an Estonian e-Residency structure, it is important to review whether Estonia is still the right place for your VAT registration strategy. Recent rule changes mean many remote-managed companies can no longer rely on Estonia as an easy route to an EU VAT ID, which can also affect where fiscal representation becomes necessary. Our guide to Estonia e-Residency VAT explains what changed, why economic substance now matters more, and what affected businesses should do next.

6. Consequences of Not Having Fiscal representation

Not appointing a fiscal representative (when required) can significantly impact your operations and finances:

- Financial Penalties and Fines

- EU tax authorities impose fines for non-compliance, which can be substantial.

- Any VAT that was paid incorrectly may not be refunded, leading to direct financial losses.

- Operational Roadblocks

- Lack of proper VAT registration could result in rejected applications to sell in certain EU countries.

- Major platforms, suppliers, or manufacturers may refuse to do business with companies that cannot prove compliance with local VAT laws.

- Reputational Damage

- Non-compliance raises red flags with local authorities, which can harm your credibility and relationships with partners in the EU market.

Not sure whether your business needs fiscal representation in the EU or whether another VAT route is enough? hellotax can review your stock locations, imports, and country-specific registration obligations. Speak to our team here.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

7. Administrative Advantages of Fiscal Representation

Simplifying VAT Processes

A fiscal representative deals directly with the tax authorities, managing VAT registration, filings, and any inquiries on your behalf. This centralized approach:

- Accelerates VAT Registration: Often completed more quickly due to established local connections.

- Minimizes Errors: Experts well-versed in local VAT laws reduce the risk of mistakes.

- Keeps You Up-to-Date: They stay current with ever-changing tax regulations, ensuring continuous compliance.

Reducing Administrative Burdens

By offloading VAT-related tasks to a fiscal representative:

- Save Time and Resources: Focus on core business activities, such as marketing and product development, rather than navigating VAT regulations.

- Reduce Risk: Less chance of misreporting or missing deadlines, which could lead to penalties.

- Holistic Approach: Many fiscal representatives offer complementary services like audit support and real-time VAT tracking, ensuring a thorough approach to compliance.

For more information about EU rules on VAT click here.

8. Understanding the Reverse Charge Mechanism

Definition and Application in VAT Compliance

Under the Reverse Charge Mechanism, the responsibility for reporting and paying VAT shifts from the seller to the buyer. This applies mainly to B2B transactions within the EU and is especially relevant if you’re a non-EU business providing services to EU-based companies or selling goods under certain conditions.

- No Need for Multiple Registrations: Because the VAT liability transfers to the buyer, the foreign seller may avoid registering in every EU country where they sell.

- Streamlined Reporting: The buyer records both the input and output VAT, simplifying the seller’s compliance obligations.

Benefits for Non-EU Businesses

- Reduced Administrative Complexity: Minimizes the number of VAT returns you need to file across different EU Member States.

- Cost Efficiency: Eliminates or reduces the need to register in certain markets, saving on administrative fees and ongoing compliance costs.

- Focus on Core Activities: Non-EU companies can concentrate on growth and expansion rather than juggling various VAT systems.

The reverse charge can reduce the number of situations where a supplier needs to account for VAT locally, but it does not remove registration or representation obligations where imports, stock storage, or local taxable supplies still create a VAT footprint.

If your business also makes cross-border B2C sales inside the EU, our guide to One Stop Shop (OSS) explains when OSS can simplify reporting and when local VAT obligations still remain.

9. Conclusion: Drive Growth in the EU Market with the Right Partner

Why Fiscal Representation is a Strategic Must

For non-EU businesses, fiscal representation in the European Union goes far beyond mere compliance. It is a strategic tool that safeguards against penalties, streamlines VAT processes, and ensures seamless interactions with local tax authorities. By choosing the right fiscal representative, you create a solid foundation for sustainable growth within the EU market.

How hellotax Can Help

At hellotax, we specialize in EU VAT compliance for online sellers, with services that include fiscal representation, VAT registration, return filing, and more. We combine professional expertise with user-friendly software solutions to keep your business compliant while reducing administrative burdens.

- Expertise in Multiple Jurisdictions: Our multilingual team understands the nuances of VAT across various EU Member States.

- All-in-One Platform: Manage your VAT registrations, filings, and communications from a single dashboard.

- Personalized Support: Tailored guidance for your specific business model—whether you’re an Amazon FBA seller, a D2C brand, or a niche marketplace vendor.

For a broader operational overview, our EU VAT Compliance Checklist for Online Sellers (2026) shows how registrations, local filings, OSS, stock movements, and tax letters fit together in practice.

Frequently Asked Questions

What is fiscal representation in the EU?

Fiscal representation in the EU means appointing a local representative to help a non-EU business meet VAT obligations such as registration, filing, payments, and tax authority communication.

When is fiscal representation in the EU required?

It may be required when a non-EU business makes taxable supplies in an EU country, imports goods there, or stores stock locally, but the exact rule depends on the Member State.

Does fiscal representation replace VAT registration?

No. Fiscal representation supports or handles VAT compliance, but it does not replace the need for VAT registration where registration is required.

Do all EU countries require fiscal representation for non-EU businesses?

No. The requirement is country-specific, which is why businesses should confirm the current rule in each Member State where they need to register.

Ready to simplify fiscal representation in the EU and reduce VAT risk across multiple countries? hellotax can help you assess where representation is required, manage registrations, and support ongoing compliance. Contact our VAT experts.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

- Having a recognized local fiscal representative fosters trust and often speeds up issue resolution with local tax offices.

- For many non-EU sellers, the real benefit is not only filing support but also having a local point of contact who can respond to tax office letters, document requests, and registration follow-up quickly and in the local language.

5. EU countries where fiscal representation is often required

Fiscal representation requirements for non-EU businesses are set at national level, so they must always be confirmed country by country. In practice, several EU Member States often require non-EU businesses to appoint a fiscal representative or local equivalent when registering for VAT, especially where imports or local stock are involved.

- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Denmark

- Estonia

- Greece

- Hungary

- Italy

- Lithuania

- Netherlands

- Poland

- Portugal

- Romania

- Slovenia

- Spain

- Sweden

Germany has a slightly different model—non-EU businesses typically must appoint a tax agent rather than a fiscal representative, although the functions are quite similar. Meanwhile, countries like France, Ireland, Finland, Latvia, Malta, Luxembourg, the Czech Republic, and Slovakia do not always require a fiscal representative, but local rules may still require some form of local agent or direct contact.

Because local rules can change, sellers should verify the current requirement before relying on a historic country list.

It’s essential to verify the requirements of each country because they can change, and exceptions may apply depending on specific business activities.

If your business was built around an Estonian e-Residency structure, it is important to review whether Estonia is still the right place for your VAT registration strategy. Recent rule changes mean many remote-managed companies can no longer rely on Estonia as an easy route to an EU VAT ID, which can also affect where fiscal representation becomes necessary. Our guide to Estonia e-Residency VAT explains what changed, why economic substance now matters more, and what affected businesses should do next.

6. Consequences of Not Having Fiscal representation

Not appointing a fiscal representative (when required) can significantly impact your operations and finances:

- Financial Penalties and Fines

- EU tax authorities impose fines for non-compliance, which can be substantial.

- Any VAT that was paid incorrectly may not be refunded, leading to direct financial losses.

- Operational Roadblocks

- Lack of proper VAT registration could result in rejected applications to sell in certain EU countries.

- Major platforms, suppliers, or manufacturers may refuse to do business with companies that cannot prove compliance with local VAT laws.

- Reputational Damage

- Non-compliance raises red flags with local authorities, which can harm your credibility and relationships with partners in the EU market.

Not sure whether your business needs fiscal representation in the EU or whether another VAT route is enough? hellotax can review your stock locations, imports, and country-specific registration obligations. Speak to our team here.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

7. Administrative Advantages of Fiscal Representation

Simplifying VAT Processes

A fiscal representative deals directly with the tax authorities, managing VAT registration, filings, and any inquiries on your behalf. This centralized approach:

- Accelerates VAT Registration: Often completed more quickly due to established local connections.

- Minimizes Errors: Experts well-versed in local VAT laws reduce the risk of mistakes.

- Keeps You Up-to-Date: They stay current with ever-changing tax regulations, ensuring continuous compliance.

Reducing Administrative Burdens

By offloading VAT-related tasks to a fiscal representative:

- Save Time and Resources: Focus on core business activities, such as marketing and product development, rather than navigating VAT regulations.

- Reduce Risk: Less chance of misreporting or missing deadlines, which could lead to penalties.

- Holistic Approach: Many fiscal representatives offer complementary services like audit support and real-time VAT tracking, ensuring a thorough approach to compliance.

For more information about EU rules on VAT click here.

8. Understanding the Reverse Charge Mechanism

Definition and Application in VAT Compliance

Under the Reverse Charge Mechanism, the responsibility for reporting and paying VAT shifts from the seller to the buyer. This applies mainly to B2B transactions within the EU and is especially relevant if you’re a non-EU business providing services to EU-based companies or selling goods under certain conditions.

- No Need for Multiple Registrations: Because the VAT liability transfers to the buyer, the foreign seller may avoid registering in every EU country where they sell.

- Streamlined Reporting: The buyer records both the input and output VAT, simplifying the seller’s compliance obligations.

Benefits for Non-EU Businesses

- Reduced Administrative Complexity: Minimizes the number of VAT returns you need to file across different EU Member States.

- Cost Efficiency: Eliminates or reduces the need to register in certain markets, saving on administrative fees and ongoing compliance costs.

- Focus on Core Activities: Non-EU companies can concentrate on growth and expansion rather than juggling various VAT systems.

The reverse charge can reduce the number of situations where a supplier needs to account for VAT locally, but it does not remove registration or representation obligations where imports, stock storage, or local taxable supplies still create a VAT footprint.

If your business also makes cross-border B2C sales inside the EU, our guide to One Stop Shop (OSS) explains when OSS can simplify reporting and when local VAT obligations still remain.

9. Conclusion: Drive Growth in the EU Market with the Right Partner

Why Fiscal Representation is a Strategic Must

For non-EU businesses, fiscal representation in the European Union goes far beyond mere compliance. It is a strategic tool that safeguards against penalties, streamlines VAT processes, and ensures seamless interactions with local tax authorities. By choosing the right fiscal representative, you create a solid foundation for sustainable growth within the EU market.

How hellotax Can Help

At hellotax, we specialize in EU VAT compliance for online sellers, with services that include fiscal representation, VAT registration, return filing, and more. We combine professional expertise with user-friendly software solutions to keep your business compliant while reducing administrative burdens.

- Expertise in Multiple Jurisdictions: Our multilingual team understands the nuances of VAT across various EU Member States.

- All-in-One Platform: Manage your VAT registrations, filings, and communications from a single dashboard.

- Personalized Support: Tailored guidance for your specific business model—whether you’re an Amazon FBA seller, a D2C brand, or a niche marketplace vendor.

For a broader operational overview, our EU VAT Compliance Checklist for Online Sellers (2026) shows how registrations, local filings, OSS, stock movements, and tax letters fit together in practice.

Frequently Asked Questions

What is fiscal representation in the EU?

Fiscal representation in the EU means appointing a local representative to help a non-EU business meet VAT obligations such as registration, filing, payments, and tax authority communication.

When is fiscal representation in the EU required?

It may be required when a non-EU business makes taxable supplies in an EU country, imports goods there, or stores stock locally, but the exact rule depends on the Member State.

Does fiscal representation replace VAT registration?

No. Fiscal representation supports or handles VAT compliance, but it does not replace the need for VAT registration where registration is required.

Do all EU countries require fiscal representation for non-EU businesses?

No. The requirement is country-specific, which is why businesses should confirm the current rule in each Member State where they need to register.

Ready to simplify fiscal representation in the EU and reduce VAT risk across multiple countries? hellotax can help you assess where representation is required, manage registrations, and support ongoing compliance. Contact our VAT experts.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

- Avoidance of Penalties

- Ensures adherence to local VAT regulations, preventing fines and penalties that can arise from non-compliance or delayed filings.

- Local Expertise

- Tax regulations and VAT rates can vary between countries. A fiscal representative’s localized knowledge helps you navigate these differences efficiently.

- Cash Flow Improvements

- Some fiscal representatives can assist in obtaining VAT deferment licenses or navigating import VAT deferrals, freeing up cash flow for your business.

- Streamlined Registration and Ongoing Compliance

- End-to-end management of VAT registration, return filings, payments, and official communications reduces administrative hassle.

- Better Relationship with Tax Authorities

- Having a recognized local fiscal representative fosters trust and often speeds up issue resolution with local tax offices.

- Local point of contact

- For many non-EU sellers, the real benefit is not only filing support but also having a local point of contact who can respond to tax office letters, document requests, and registration follow-up quickly and in the local language.

5. EU countries where fiscal representation is often required

Fiscal representation requirements for non-EU businesses are set at national level, so they must always be confirmed country by country. In practice, several EU Member States often require non-EU businesses to appoint a fiscal representative or local equivalent when registering for VAT, especially where imports or local stock are involved.

- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Denmark

- Estonia

- Greece

- Hungary

- Italy

- Lithuania

- Netherlands

- Poland

- Portugal

- Romania

- Slovenia

- Spain

- Sweden

Germany has a slightly different model—non-EU businesses typically must appoint a tax agent rather than a fiscal representative, although the functions are quite similar. Meanwhile, countries like France, Ireland, Finland, Latvia, Malta, Luxembourg, the Czech Republic, and Slovakia do not always require a fiscal representative, but local rules may still require some form of local agent or direct contact.

Because local rules can change, sellers should verify the current requirement before relying on a historic country list.

It’s essential to verify the requirements of each country because they can change, and exceptions may apply depending on specific business activities.

If your business was built around an Estonian e-Residency structure, it is important to review whether Estonia is still the right place for your VAT registration strategy. Recent rule changes mean many remote-managed companies can no longer rely on Estonia as an easy route to an EU VAT ID, which can also affect where fiscal representation becomes necessary. Our guide to Estonia e-Residency VAT explains what changed, why economic substance now matters more, and what affected businesses should do next.

6. Consequences of Not Having Fiscal representation

Not appointing a fiscal representative (when required) can significantly impact your operations and finances:

- Financial Penalties and Fines

- EU tax authorities impose fines for non-compliance, which can be substantial.

- Any VAT that was paid incorrectly may not be refunded, leading to direct financial losses.

- Operational Roadblocks

- Lack of proper VAT registration could result in rejected applications to sell in certain EU countries.

- Major platforms, suppliers, or manufacturers may refuse to do business with companies that cannot prove compliance with local VAT laws.

- Reputational Damage

- Non-compliance raises red flags with local authorities, which can harm your credibility and relationships with partners in the EU market.

Not sure whether your business needs fiscal representation in the EU or whether another VAT route is enough? hellotax can review your stock locations, imports, and country-specific registration obligations. Speak to our team here.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

7. Administrative Advantages of Fiscal Representation

Simplifying VAT Processes

A fiscal representative deals directly with the tax authorities, managing VAT registration, filings, and any inquiries on your behalf. This centralized approach:

- Accelerates VAT Registration: Often completed more quickly due to established local connections.

- Minimizes Errors: Experts well-versed in local VAT laws reduce the risk of mistakes.

- Keeps You Up-to-Date: They stay current with ever-changing tax regulations, ensuring continuous compliance.

Reducing Administrative Burdens

By offloading VAT-related tasks to a fiscal representative:

- Save Time and Resources: Focus on core business activities, such as marketing and product development, rather than navigating VAT regulations.

- Reduce Risk: Less chance of misreporting or missing deadlines, which could lead to penalties.

- Holistic Approach: Many fiscal representatives offer complementary services like audit support and real-time VAT tracking, ensuring a thorough approach to compliance.

For more information about EU rules on VAT click here.

8. Understanding the Reverse Charge Mechanism

Definition and Application in VAT Compliance

Under the Reverse Charge Mechanism, the responsibility for reporting and paying VAT shifts from the seller to the buyer. This applies mainly to B2B transactions within the EU and is especially relevant if you’re a non-EU business providing services to EU-based companies or selling goods under certain conditions.

- No Need for Multiple Registrations: Because the VAT liability transfers to the buyer, the foreign seller may avoid registering in every EU country where they sell.

- Streamlined Reporting: The buyer records both the input and output VAT, simplifying the seller’s compliance obligations.

Benefits for Non-EU Businesses

- Reduced Administrative Complexity: Minimizes the number of VAT returns you need to file across different EU Member States.

- Cost Efficiency: Eliminates or reduces the need to register in certain markets, saving on administrative fees and ongoing compliance costs.

- Focus on Core Activities: Non-EU companies can concentrate on growth and expansion rather than juggling various VAT systems.

The reverse charge can reduce the number of situations where a supplier needs to account for VAT locally, but it does not remove registration or representation obligations where imports, stock storage, or local taxable supplies still create a VAT footprint.

If your business also makes cross-border B2C sales inside the EU, our guide to One Stop Shop (OSS) explains when OSS can simplify reporting and when local VAT obligations still remain.

9. Conclusion: Drive Growth in the EU Market with the Right Partner

Why Fiscal Representation is a Strategic Must

For non-EU businesses, fiscal representation in the European Union goes far beyond mere compliance. It is a strategic tool that safeguards against penalties, streamlines VAT processes, and ensures seamless interactions with local tax authorities. By choosing the right fiscal representative, you create a solid foundation for sustainable growth within the EU market.

How hellotax Can Help

At hellotax, we specialize in EU VAT compliance for online sellers, with services that include fiscal representation, VAT registration, return filing, and more. We combine professional expertise with user-friendly software solutions to keep your business compliant while reducing administrative burdens.

- Expertise in Multiple Jurisdictions: Our multilingual team understands the nuances of VAT across various EU Member States.

- All-in-One Platform: Manage your VAT registrations, filings, and communications from a single dashboard.

- Personalized Support: Tailored guidance for your specific business model—whether you’re an Amazon FBA seller, a D2C brand, or a niche marketplace vendor.

For a broader operational overview, our EU VAT Compliance Checklist for Online Sellers (2026) shows how registrations, local filings, OSS, stock movements, and tax letters fit together in practice.

Frequently Asked Questions

What is fiscal representation in the EU?

Fiscal representation in the EU means appointing a local representative to help a non-EU business meet VAT obligations such as registration, filing, payments, and tax authority communication.

When is fiscal representation in the EU required?

It may be required when a non-EU business makes taxable supplies in an EU country, imports goods there, or stores stock locally, but the exact rule depends on the Member State.

Does fiscal representation replace VAT registration?

No. Fiscal representation supports or handles VAT compliance, but it does not replace the need for VAT registration where registration is required.

Do all EU countries require fiscal representation for non-EU businesses?

No. The requirement is country-specific, which is why businesses should confirm the current rule in each Member State where they need to register.

Ready to simplify fiscal representation in the EU and reduce VAT risk across multiple countries? hellotax can help you assess where representation is required, manage registrations, and support ongoing compliance. Contact our VAT experts.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

Fiscal representation in the EU is often a key VAT issue for non-EU businesses selling goods or services into Europe. In this guide, we explain when fiscal representation may be required, how it differs from other VAT support models, which EU countries often require it, and what online sellers should check in 2026 before registering or importing goods.

Need help with fiscal representation in the EU? hellotax can review your VAT setup, registration needs, and country-specific representation requirements. Contact our VAT experts.

Whether you are an Amazon seller, an eCommerce entrepreneur using various marketplaces, or a direct-to-consumer brand shipping goods to multiple EU countries, understanding how fiscal representation works is a must for ensuring compliance and maximizing profitability.

1. When Is Fiscal Representation in the EU Necessary for Non-EU Businesses?

Fiscal representation in the EU may become necessary for non-EU businesses when they make taxable supplies in an EU Member State, import goods into the EU for sale, or store stock locally through warehouses or fulfilment networks. However, the requirement is not the same in every country, so businesses should always confirm the rule in the Member State where VAT registration is needed.

In some EU countries, businesses established in countries with mutual assistance arrangements, including the UK, may be treated more favourably than other non-EU businesses for VAT representation purposes. However, the exact requirement still depends on the Member State, so it should always be checked locally.

If you first need to understand where VAT registration is required before fiscal representation even becomes relevant, our guide to EU VAT Registration for Non-EU Businesses explains the main triggers for non-EU sellers.

2. Definition of Fiscal representation in the EU

A fiscal representative is a specialized individual or entity, authorized to act on behalf of a non-EU business in fulfilling VAT obligations within EU countries. Their main responsibilities include:

- VAT Registration: Managing the entire registration process with the local tax authority.

- VAT Returns: Preparing and filing periodic VAT returns.

- VAT Payments: Ensuring timely payment of VAT liabilities.

- Communication: Handling all correspondence with tax authorities, including any audits, inquiries, or official notifications.

By assigning these responsibilities to a fiscal representative, non-resident companies can more easily adapt to complex EU regulations and avoid costly mistakes.

3. General vs. Limited Fiscal Representation

There are two primary types of fiscal representation: general and limited.

General Representation

- Comprehensive Service: The fiscal representative manages all aspects of VAT compliance—registration, returns, payments, and communication with tax authorities.

- Higher Responsibility: Because the representative assumes full liability for VAT obligations, a bank guarantee or insurance bond may be required.

- Ideal For: Businesses with substantial or ongoing activities in the EU that require end-to-end VAT compliance support.

Limited Representation

- Selective Tasks: The fiscal representative handles specific VAT obligations (e.g., filing returns only, or managing VAT payments but not returns).

- Flexibility: This approach allows non-EU businesses to retain control over some aspects of VAT compliance.

- Lower Guarantee Requirements: Bank guarantees, if needed, are typically lower than in general representation.

- Ideal For: Businesses with limited or occasional operations in the EU, or those testing the market.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

4. Benefits of Appointing a Fiscal Representative in the EU

Working with a fiscal representative provides multiple advantages, especially for non-EU companies selling in diverse EU markets:

- Avoidance of Penalties

- Ensures adherence to local VAT regulations, preventing fines and penalties that can arise from non-compliance or delayed filings.

- Local Expertise

- Tax regulations and VAT rates can vary between countries. A fiscal representative’s localized knowledge helps you navigate these differences efficiently.

- Cash Flow Improvements

- Some fiscal representatives can assist in obtaining VAT deferment licenses or navigating import VAT deferrals, freeing up cash flow for your business.

- Streamlined Registration and Ongoing Compliance

- End-to-end management of VAT registration, return filings, payments, and official communications reduces administrative hassle.

- Better Relationship with Tax Authorities

- Having a recognized local fiscal representative fosters trust and often speeds up issue resolution with local tax offices.

- Local point of contact

- For many non-EU sellers, the real benefit is not only filing support but also having a local point of contact who can respond to tax office letters, document requests, and registration follow-up quickly and in the local language.

5. EU countries where fiscal representation is often required

Fiscal representation requirements for non-EU businesses are set at national level, so they must always be confirmed country by country. In practice, several EU Member States often require non-EU businesses to appoint a fiscal representative or local equivalent when registering for VAT, especially where imports or local stock are involved.

- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Denmark

- Estonia

- Greece

- Hungary

- Italy

- Lithuania

- Netherlands

- Poland

- Portugal

- Romania

- Slovenia

- Spain

- Sweden

Germany has a slightly different model—non-EU businesses typically must appoint a tax agent rather than a fiscal representative, although the functions are quite similar. Meanwhile, countries like France, Ireland, Finland, Latvia, Malta, Luxembourg, the Czech Republic, and Slovakia do not always require a fiscal representative, but local rules may still require some form of local agent or direct contact.

Because local rules can change, sellers should verify the current requirement before relying on a historic country list.

It’s essential to verify the requirements of each country because they can change, and exceptions may apply depending on specific business activities.

If your business was built around an Estonian e-Residency structure, it is important to review whether Estonia is still the right place for your VAT registration strategy. Recent rule changes mean many remote-managed companies can no longer rely on Estonia as an easy route to an EU VAT ID, which can also affect where fiscal representation becomes necessary. Our guide to Estonia e-Residency VAT explains what changed, why economic substance now matters more, and what affected businesses should do next.

6. Consequences of Not Having Fiscal representation

Not appointing a fiscal representative (when required) can significantly impact your operations and finances:

- Financial Penalties and Fines

- EU tax authorities impose fines for non-compliance, which can be substantial.

- Any VAT that was paid incorrectly may not be refunded, leading to direct financial losses.

- Operational Roadblocks

- Lack of proper VAT registration could result in rejected applications to sell in certain EU countries.

- Major platforms, suppliers, or manufacturers may refuse to do business with companies that cannot prove compliance with local VAT laws.

- Reputational Damage

- Non-compliance raises red flags with local authorities, which can harm your credibility and relationships with partners in the EU market.

Not sure whether your business needs fiscal representation in the EU or whether another VAT route is enough? hellotax can review your stock locations, imports, and country-specific registration obligations. Speak to our team here.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

7. Administrative Advantages of Fiscal Representation

Simplifying VAT Processes

A fiscal representative deals directly with the tax authorities, managing VAT registration, filings, and any inquiries on your behalf. This centralized approach:

- Accelerates VAT Registration: Often completed more quickly due to established local connections.

- Minimizes Errors: Experts well-versed in local VAT laws reduce the risk of mistakes.

- Keeps You Up-to-Date: They stay current with ever-changing tax regulations, ensuring continuous compliance.

Reducing Administrative Burdens

By offloading VAT-related tasks to a fiscal representative:

- Save Time and Resources: Focus on core business activities, such as marketing and product development, rather than navigating VAT regulations.

- Reduce Risk: Less chance of misreporting or missing deadlines, which could lead to penalties.

- Holistic Approach: Many fiscal representatives offer complementary services like audit support and real-time VAT tracking, ensuring a thorough approach to compliance.

For more information about EU rules on VAT click here.

8. Understanding the Reverse Charge Mechanism

Definition and Application in VAT Compliance

Under the Reverse Charge Mechanism, the responsibility for reporting and paying VAT shifts from the seller to the buyer. This applies mainly to B2B transactions within the EU and is especially relevant if you’re a non-EU business providing services to EU-based companies or selling goods under certain conditions.

- No Need for Multiple Registrations: Because the VAT liability transfers to the buyer, the foreign seller may avoid registering in every EU country where they sell.

- Streamlined Reporting: The buyer records both the input and output VAT, simplifying the seller’s compliance obligations.

Benefits for Non-EU Businesses

- Reduced Administrative Complexity: Minimizes the number of VAT returns you need to file across different EU Member States.

- Cost Efficiency: Eliminates or reduces the need to register in certain markets, saving on administrative fees and ongoing compliance costs.

- Focus on Core Activities: Non-EU companies can concentrate on growth and expansion rather than juggling various VAT systems.

The reverse charge can reduce the number of situations where a supplier needs to account for VAT locally, but it does not remove registration or representation obligations where imports, stock storage, or local taxable supplies still create a VAT footprint.

If your business also makes cross-border B2C sales inside the EU, our guide to One Stop Shop (OSS) explains when OSS can simplify reporting and when local VAT obligations still remain.

9. Conclusion: Drive Growth in the EU Market with the Right Partner

Why Fiscal Representation is a Strategic Must

For non-EU businesses, fiscal representation in the European Union goes far beyond mere compliance. It is a strategic tool that safeguards against penalties, streamlines VAT processes, and ensures seamless interactions with local tax authorities. By choosing the right fiscal representative, you create a solid foundation for sustainable growth within the EU market.

How hellotax Can Help

At hellotax, we specialize in EU VAT compliance for online sellers, with services that include fiscal representation, VAT registration, return filing, and more. We combine professional expertise with user-friendly software solutions to keep your business compliant while reducing administrative burdens.

- Expertise in Multiple Jurisdictions: Our multilingual team understands the nuances of VAT across various EU Member States.

- All-in-One Platform: Manage your VAT registrations, filings, and communications from a single dashboard.

- Personalized Support: Tailored guidance for your specific business model—whether you’re an Amazon FBA seller, a D2C brand, or a niche marketplace vendor.

For a broader operational overview, our EU VAT Compliance Checklist for Online Sellers (2026) shows how registrations, local filings, OSS, stock movements, and tax letters fit together in practice.

Frequently Asked Questions

What is fiscal representation in the EU?

Fiscal representation in the EU means appointing a local representative to help a non-EU business meet VAT obligations such as registration, filing, payments, and tax authority communication.

When is fiscal representation in the EU required?

It may be required when a non-EU business makes taxable supplies in an EU country, imports goods there, or stores stock locally, but the exact rule depends on the Member State.

Does fiscal representation replace VAT registration?

No. Fiscal representation supports or handles VAT compliance, but it does not replace the need for VAT registration where registration is required.

Do all EU countries require fiscal representation for non-EU businesses?

No. The requirement is country-specific, which is why businesses should confirm the current rule in each Member State where they need to register.

Ready to simplify fiscal representation in the EU and reduce VAT risk across multiple countries? hellotax can help you assess where representation is required, manage registrations, and support ongoing compliance. Contact our VAT experts.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!