Dropshipping is a delivery or fulfillment method that allows retailers to set up and run a business without large investments, since products are only purchased from the supplier after they have been sold to the end customer. But dropshipping brings with it some complications, especially when it comes to VAT compliance for dropshipping. Understanding the VAT obligations in different countries is essential to remain compliant and avoid penalties.. In the following article, you will find out what you have to consider in terms of VAT compliance for dropshipping. We will also explain why OSS is not an option for dropshippers as it would jeopardise your dropshipping scheme.

Maria

Last Updated on 10 October 2024

Definition of dropshipping in VAT law

Dropshipping is also known as direct selling or drop shipping. From a VAT point of view, however, VAT compliance for dropshipping categorizes the model as a “chain transaction”. Chain transactions are defined as all transactions with a product that are subject to VAT in which at least three people are involved, and the shipment is made from the first entrepreneur to the last customer.

This is exactly the case with dropshipping, as the dropshipper acts as an intermediary and second link between the supplier or manufacturer and the end customer, although according to the VAT definition of chain transactions, several intermediaries can also be involved.

The alternative to chain transactions is traditional retail, whether online or stationary. In this case, the online retailer buys the products in advance, stores them, and sells and ships them directly to the end customer. In both cases, however, the transactions are usually subject to VAT.

In classic retail, not dropshipping, the retailer would purchase their products from the manufacturer and only then sell and ship them. In this case, the purchase from the manufacturer in Germany would be typically taxed at 19% although other rates could be applied depending on the case, which the retailer could then report as input tax.

The retailer would then ship the products to France. In terms of VAT, there would be three options to process this transaction:

- If the entrepreneur’s EU-wide cross-border turnover is below the EU-wide delivery threshold, the transaction is taxed at the German VAT rate of 19% and listed in a German VAT return.

- If the entrepreneur’s EU-wide cross-border turnover is above the EU-wide delivery threshold, the transaction will be taxed at the French VAT rate of 20% and listed in a French VAT return. To do this, the seller must register for VAT in France.

- If the seller uses the One-Stop-Shop, the French VAT rate of 20% is used regardless of the total turnover. However, the transaction is listed in the OSS report and no additional VAT registration is required.

How hellotax can help you with dropshipping

During a free consultation with our VAT specialists, we will explain how you can ensure VAT compliance for dropshipping based on your sales flows, fulfillment methods, and target markets. It is important to note that for dropshippers, the One-Stop-Shop (OSS) is not a viable option. Contrary to common misconceptions, only local VAT registrations and ongoing VAT filings in the countries where you conduct your sales will make you VAT compliant.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

VAT liability for dropshipping

VAT is always due when a company generates sales. Understanding VAT compliance for dropshipping requires knowing when and how VAT applies in different scenarios. At first glance, this sounds quite simple, but there are a few exceptions and special regulations that complicate VAT liability. Whether or not and how much VAT has to be paid can depend on several factors:

- Type of products

- Customers

- Location of customers

- Annual turnover of the company

The type of products, customers, and annual turnover of the company always play a role. Some products are subject to reduced VAT rates in many countries, a distinction is usually made between sales to companies and private individuals, and in many countries, there are special regulations for entrepreneurs with low sales. With dropshipping, however, the locations of the customer and the supplier are additionally important. According to the classic location rule for deliveries, the place of delivery is where the transport to the customer begins.

In contrast, according to the mail order delivery rules, the place of delivery is where the transport to the customer ends, i.e., in the customer’s home country. The place of delivery determines the applicable VAT rates and VAT regulations to be followed. However, dropshipping or chain transactions formally consist of several deliveries and therefore contain some exceptions. These are best illustrated with a few examples.

Navigating VAT compliance for dropshipping means understanding how cross-border transactions, B2C rules, and supply chain roles affect your obligations in each EU country.

VAT changes in 2021

But first, some VAT changes have to be discussed. Because in July 2021 the EU-wide VAT law was updated. The following changes affect all cross-border transactions with private customers within Europe and thus not only normal mail order companies but also dropshippers.

- Country-specific delivery thresholds for the B2C mail order business, which, if exceeded, resulted in a VAT registration obligation in the respective country, were replaced by an EU-wide delivery threshold, after which sellers must register for VAT in all countries in which their end customers are based.

- Alternatively, sellers can register for the One-Stop-Shop (OSS). All EU foreign VAT registrations are thus obsolete and transactions are settled via a uniform OSS report in the home country. However, registrations are still necessary if goods are stored in other EU countries.

Import VAT limits, such as the German limit, which was set at a maximum value of goods of €22, were removed without replacement. From now on, all goods, regardless of their value, are subject to import VAT when imported into the European Union. The Import-One-Stop-Shop (IOSS) offers a way of simplifying the reporting of import VAT across the EU.

The following practical examples illustrate how VAT compliance for dropshipping varies depending on where the supplier, seller, and end customer are based:

Scenario 1: VAT on dropshipping in a single country

The VAT situation is easiest when all parties involved are based in one country, for example when the supplier, dropshipper, and end customer live or are registered in Germany. In this case, all invoices contain the German VAT rates. However, the dropshipper can deduct the VAT calculated by the supplier as input tax in his German VAT return.

Scenario 2: VAT for dropshipping with delivery from the home country

In this example, a German dropshipper sells products subject to normal VAT rates to a French end customer. He obtains his products from a supplier in Germany.

In classic dropshipping, the German manufacturer or supplier sends the goods directly to the end customer in France and is therefore the first link in the chain transaction. Since the end customer is based in Europe and the shipment crosses national borders, this delivery is considered an intra-community shipment and therefore tax-free. The invoice from the supplier to the dropshipper, therefore, also does not contain any VAT and the dropshipper cannot deduct input tax.

Now the second link, the dropshipper, comes into play as a middleman. He is also formally considered a supplier in chain transactions – as the supplier of the invoice. Since this is a chain transaction, the delivery threshold regulation does not apply here. The invoice to the end customer should therefore immediately include the French VAT rate of 20%. Therefore the dropshipper must VAT register in France.

In this case, you would need a French VAT registration. Hellotax can help you with your French VAT returns. The dropshipper would, of course, also need to file regular VAT returns in their home country Germany.

Scenario 3 : VAT for dropshipping with delivery from a another EU country

Dropshipping also often involves three parties from three different countries. For example, a German dropshipper could source a product from a Polish supplier and sell it to a French customer. In this case, too, the invoice between the supplier and the dropshipper does not include VAT. Because both entrepreneurs are based in different EU countries and it is a B2B transaction, the VAT is processed using the reverse charge procedure.

VAT would only apply where the final customer is based, that is France.

As previously, you will need a French VAT ID. hellotax can take care of your registration and VAT returns.

Scenario 4: VAT for dropshipping with delivery from abroad

When dropshipping products to customers in Europe from manufacturers outside the EU, VAT compliance takes on an additional layer of complexity. Once the goods enter the European Union, the question of who handles customs duties and taxes at the border becomes crucial.

The responsibility for VAT and customs payments depends on who is designated as the importer of record. In some instances, the end customer may bear this responsibility, paying the necessary fees through a freight company. This should always be agreed upon by the parties. Otherwise, the customers could find themselves having to pay the extra tax and customs obligations without having been made aware previously.

These examples highlight how important it is to ensure full VAT compliance for dropshipping when operating across multiple jurisdictions.

Do you find the scenarios too complex to deal with? Contact us today and we will guide you smoothly through the process. We are experts on VAT compliance for dropshippers.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!

VAT rates in Europe

When it comes to VAT in European countries, a distinction is first made between physical and digital goods. The former are products that are packaged and shipped, such as clothing and electronics. Examples of the latter would be e-books, music downloads, stock photos, and webinars.

For dropshipping, however, only the VAT rates for physical products are relevant. Furthermore, the VAT rates differ between certain product categories. In Germany, reduced tax rates apply to books and food, for example. However, each EU country has its own reduced tax rates applied to decorations, study materials, and more.

Until recently, dropshippers were able to add domestic VAT rates to transactions with end consumers located in other EU countries. Country-specific, mostly very high delivery thresholds for the B2C mail order business applied. Only after crossing the country-specific thresholds, e.g. the Dutch one of 100,000€, though sales to customers in that one country only country-specific VAT rates had to be applied. That changed on July 1, 2021.

On this day, country-specific delivery thresholds were replaced by an EU-wide, low threshold of just €10,000. This limit is reached through all cross-border B2C transactions combined and, therefore, crossed much earlier. For classic mail-order companies and also dropshippers, this means that they now have to deal more frequently with EU VAT rates. Your sales system must be able to map the VAT regulations and country-specific tax rates, both the normal and all reduced ones. Sellers and dropshippers also have to adjust their prices. German customers are only charged 19% VAT, while Hungarian customers pay 27%, for example. Be aware that the seller must also register for VAT in the other relevant EU country.

Being aware of country-specific VAT rates is another crucial component of maintaining proper VAT compliance for dropshipping.

VAT IDs for Dropshippers vs. OSS

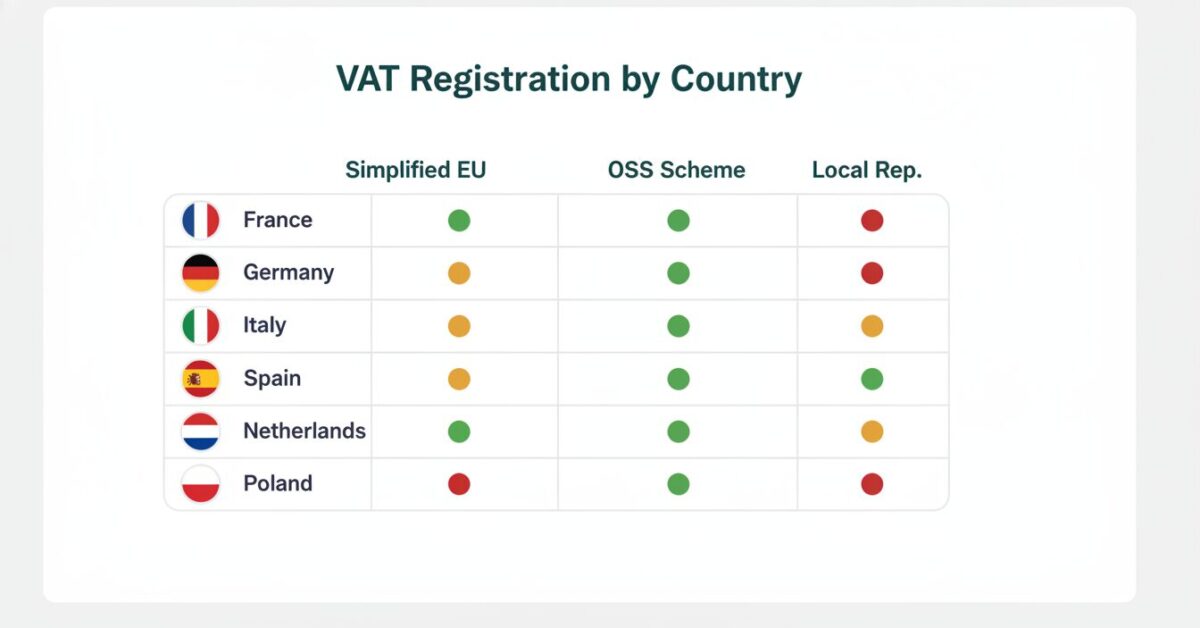

A lot has changed here since the delivery threshold for mail orders was revised and the One-Stop-Shop was introduced. Dropshippers with cross-border transactions with European private customers must now register for VAT and obtain VAT identification numbers (VAT ID) in all EU countries, in which their customers are based.

It has become common practice for dropshippers to use OSS for the VAT obligations as many local accountants and tax compliance services are advising wrongly to do so.As explained in this article, this will not make you compliant as, according to current rules, you will still need to register for VAT in every single EU country where you intend to sell. For more detailed information please read through this article on dropshipping and OSS which fully develops the topic.

Understanding the difference between OSS and local registrations is vital for achieving long-term VAT compliance for dropshipping in the EU.

If you want a wider overview beyond dropshipping-specific issues, see our EU VAT compliance guide.

Import VAT when dropshipping with IOSS

The regular VAT that must be added to the price when selling goods to end consumers is not the only VAT that dropshippers have to worry about. The dropshipping business model is often associated with foreign, but especially Chinese suppliers – and with good reason. The vast majority of dropshippers source their products from abroad and thus benefit from low production prices. However, there is an import VAT due when importing the products into Europe.

Here, too, a lot has changed on July 1, 2021. So far, for example, deliveries with a maximum goods value of €22, or effectively €26.30 thanks to calculatory flexibility, were exempt from import VAT in Germany. This exemption limit was abolished with the introduction of the new VAT system and the new delivery threshold. From July 2021 on, all products are subject to import VAT. The normal VAT rates of the importing countries apply.

But the European Union has also introduced a system for imports: the Import-One-Stop-Shop (IOSS). The IOSS is not the same as the OSS, but the procedures are similar since the latter was developed on the basis of the IOSS. If you use the IOSS, you simplify the reporting of your imports with the collected EU-wide IOSS report.

In addition to VAT for imports into the European Union, there are also country-specific customs duties that depend on the country of import. Customs duties were and are still only due from a goods value of 150€ – in Germany. Customs borders and customs fees differ from country to country and between individual product categories, but generally only apply to higher-priced deliveries.

The registered importer or importer of record (IOR) is responsible for customs duties and import VAT. With dropshipping, this is generally the customer, as he is the direct recipient of the goods from non-EU countries. The end customer must therefore pay these fees by post or directly to customs. This should be pointed out during the payment process in the dropshipping shop in order to avoid negative customer reviews.

Alternatively, the dropshipper can apply for himself to be considered a registered importer and include the fees in the purchase price. However, this is only possible without any problems if he receives the goods himself – which in turn does not correspond to the classic dropshipping model.

To support your understanding of EU tax rules when running a dropshipping business, you can refer to the official guidance provided by the European Commission’s Taxation & Customs portal. This resource offers up‑to‑date information on VAT regulations, cross‑border trade, and import rules—crucial foundations for achieving solid VAT compliance for dropshipping across multiple European countries. 👉 Visit the European Commission – Taxation & Customs VAT portal

VAT complications and accounting Income Tax for Dropshippers

Of course, VAT, import VAT, and customs duties are not the only taxes dropshippers have to pay. As the owner of a dropshipping business, like most entrepreneurs based in Europe, you are subject to income tax. However, the laws, tax rates, and special regulations differ from country to country.

In Germany, for example, you are subject to unlimited VAT liability if you not only have your registered office but also your permanent place of residence in Germany. Furthermore, the world income principle applies, according to which all income generated worldwide, i.e. sales to customers worldwide, are taxable. Similar regulations also apply in other EU countries. If you have questions about income tax, you should consult a regular tax advisor.

VAT complications and accounting in dropshipping

Income tax regulations are considered complicated by both employees and entrepreneurs. VAT, however, is a lot more complex. First of all, all business processes must be documented precisely. In addition, accounting should be handled with good software programs that can map the different source and destination countries and the complex business processes. If you have any questions about the processes in the dropshipping business from a VAT perspective, hellotax can help you.

We specialize in VAT compliance for dropshipping, Amazon sellers, and other e-commerce retailers and take care of all the necessary registrations and submissions. We are able to do this thanks to our self-developed VAT software, with which you always have an overview of your transactions and a team of specialized local tax advisors. The latter will also be happy to clarify any individual questions you may have about VAT when it comes to dropshipping. Contact us today and learn more about our services.

Whether you’re just starting out or scaling internationally, your success depends in part on strong VAT compliance for dropshipping strategies.

Book a free consultation

Our VAT experts are happy to help you. Book a free consultation today!